Introduction

Alberta’s proposed “Care First” auto insurance system is being sold as a fix for high premiums. The UCP Government’s message is simple: lower costs, faster care, less friction. Everybody is happy!

But when you read the actual actuarial costing from the Automobile Insurance Rate Board (AIRB), a different picture emerges.

This system does not reduce costs by becoming more efficient. It reduces costs by replacing individualized compensation with standardized benefits that are typically lower than what courts may award—and by limiting their ability to challenge insurers in court.

That is not a minor adjustment. That is a fundamental shift in justice and who the system is designed to serve.

What Is the AIRB—and Why Its Report Matters

The Automobile Insurance Rate Board (AIRB) regulates auto insurance rates in Alberta. It reviews insurer filings and evaluates whether premiums are justified based on actuarial data.

Its recent report on Care First is not just technical analysis. It is the financial blueprint for how the new system will work.

And the key takeaway is clear:

- Lower insurer costs

- Reduced claims payouts

- Fewer legal disputes

Those are not side effects. They are the design.

What “Care First” Actually Changes

This Is Not a Small Reform

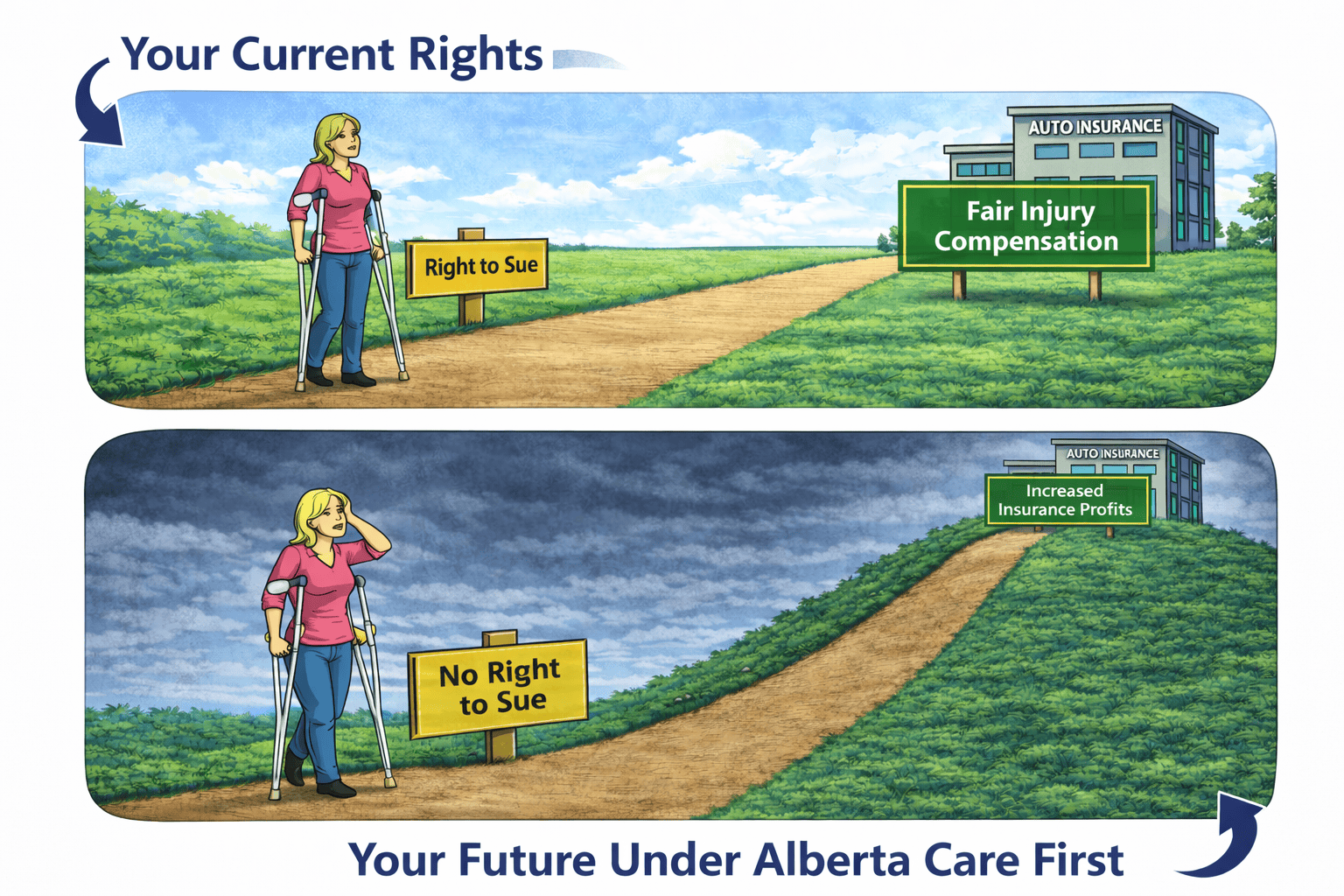

Care First replaces Alberta’s fault-based system with a no-fault model.

That means:

- You claim benefits from your own insurer

- You generally cannot sue the at-fault driver

- Compensation is replaced with predefined benefits

The system moves away from individualized justice and toward standardized payouts.

Where the “Savings” Come From

The AIRB report projects cost reductions across the system. But those savings come from three specific changes.

1. Paying Less to Injured People

Under the current system, injured Albertans can claim:

- Pain and suffering

- Income loss (past and future)

- Cost of future care

- Loss of earning capacity

Under Care First:

- Many of these claims are eliminated

- Others are capped or replaced with fixed benefits

This is the core truth: if the system will cost less it will be because it pays less. Everything else is secondary.

2. Eliminating Most Lawsuits

Lawsuits are restricted to narrow, exceptional circumstances.

This has two direct effects:

- Insurers face fewer challenges

- Injured individuals lose negotiating power

The AIRB treats this as a cost saving. It is also a shift in leverage and balance of power.

The individual’s power is reduced. The power of the billion-dollar insurance industry is increased. The Alberta Civil Trial Lawyers Association (ACTLA) similarly warns that restricting access to the courts removes a critical layer of accountability and shifts decision-making power toward insurers and administrative systems.

3. Tightening Control Over Claims

Care First introduces:

- Standardized benefit schedules

- Medical oversight frameworks

- Administrative dispute systems

These changes increase predictability—for insurers. The same changes will be a straitjacket, limiting the options of the most vulnerable people in an injury claim: the injury victims!

When Can You Still Go to Court?

Let’s be precise.

The right to sue is not completely eliminated. But it is restricted to narrow, exceptional circumstances.

The General Rule

Under the proposed model, almost all injury claims are expected to be handled outside the courts, where the balance of power favours insurers, not claimants.

This includes:

- Soft tissue injuries

- Chronic pain cases

- Many orthopedic injuries

- Most psychological injuries

These cases will be handled entirely within the insurance system.

The Exceptions—And Why They Matter

1. Catastrophic Injuries Only (In Most Cases)

Limited court access may remain for individuals with catastrophic impairments, such as:

- Severe traumatic brain injuries

- Complete spinal cord injuries

- Major amputations

But:

- The definition of “catastrophic” is strict

- It requires complex medical evidence

- Many serious injuries will not qualify

No one wishes a catastrophic injury on anyone.

If you are seriously injured—but not “catastrophically injured as strictly defined by Care First”—you are likely out of the court system entirely.

2. Unusual or Cross-Border Cases

Some claims may proceed where:

- The at-fault driver is from outside Alberta

- Coverage falls outside the Care First system

These cases are rare and do not apply to most Albertans.

3. Disputes With Your Own Insurer

Disputes with insurers do not disappear under Care First. The settlement of disputes moves.

You may still challenge:

- Denied treatment

- Cut-off benefits

- Medical assessments

But these disputes are expected to be handled through:

- Tribunals

- Internal insurer processes

Crucially, disputes will not be handled by the courts—they will be diverted into administrative processes. Access to judicial review, in those rare circumstances when it is available, will be delayed.

4. Constitutional Challenges

Yes, you can challenge the system itself.

No, this is not realistic for most people.

These cases require:

- Significant funding

- Years of litigation

- Specialized legal teams

Who Can Actually Afford to Go to Court?

Even where court access exists, very few people will be able to use it.

The Cost of a Lawsuit

A serious injury case can require:

- $5,000–$20,000+ in medical reports

- Expert witnesses

- Economic loss analysis

- Extensive legal preparation

Under the current system, those costs can be justified by the potential recovery. Good injury lawyers know when an insurance company is shortchanging an injury victim. They take case cases with an expectation of winning and recovering costs while earning more compensation for their clients.

Under Care First, injury victims and injury lawyers will have to take a huge risk in a system that is, in practice, stacked against them—ironically a system called Care First.

The Economics Change Everything

This is the part most people miss.

Even if a lawsuit is technically allowed:

- Damages are limited

- Recovery is reduced

- Risk increases

That means:

- Fewer lawyers can take cases

- Fewer cases are financially viable

- Fewer injured people get representation

The Alberta Civil Trial Lawyers Association (ACTLA) warns that limiting compensation and restricting legal rights can make it economically impractical for injured individuals to pursue claims—even where serious harm has occurred. Care First does not just limit lawsuits. It removes access to the court-based system of justice for most injury claims and the economic foundation that makes them possible.

Who Still Has Access to the Courts?

In practical terms, court access will be limited to:

Catastrophic Injury Cases

Where:

- Lifetime losses are extremely high

- The case meets strict thresholds

- The economics justify litigation

Even here, access is not guaranteed.

High-Value, Clear Cases

Rare situations where:

- Liability is clear

- Losses are substantial

- The claim fits within an exception

These will be the minority.

System-Level Challenges

Cases brought to:

- Test the law

- Define thresholds

- Challenge the system

These are not typical claims. They are strategic litigation. The costs are high.

Care First: Who Benefits—and Who Pays

Let’s be direct.

Who Benefits

- Insurance companies (lower payouts, fewer lawsuits)

- Actuarial models (predictable costs)

- Administrative systems (controlled outcomes)

Who Pays

- Injured Albertans who fall outside “catastrophic” definitions

- Families dealing with long-term financial loss

- Anyone who needs full compensation to rebuild their life

The system does not eliminate costs. It shifts more of the financial burden—from insurers to injured people.

The Premium Question

The justification for Care First is lower premiums.

But:

- The AIRB does not guarantee savings will reach consumers

- Insurers retain control over pricing

- Evidence from other regions is mixed

As a recent CBC report notes, experts continue to question whether these projected savings will meaningfully reduce premiums.

Why This Matters More Than It Sounds

Care First is not just a technical reform.

It changes:

- Your right to compensation

- Your ability to challenge insurers

- Your access to the courts

Before Care First:

- You could pursue a claim

- Compensation reflected your actual loss

- Legal action created accountability

After Care First:

- Most claims never reach court

- Compensation is standardized

- Almost all disputes are controlled within the system

The Bottom Line

Here is the accurate, plain-language reality:

Under Care First, injury claims can proceed through the courts only in narrow, exceptional circumstances—primarily involving catastrophic injuries or unusual legal situations. For most Albertans, the right to sue will be effectively removed. Even where it remains, financial and legal barriers will limit access to a small number of cases—and primarily those cases where the high financial stakes may justify the cost of litigation.

Care First is not a minor policy change. It is a shift in who the system is designed to protect.

Conclusion

The AIRB report claims that Care First will reduce costs.

It does not show that it will deliver justice.

If you want to understand Care First, do not ask how much the system saves. Ask who pockets the savings.